Know Your Customer (KYC) compliance is the backbone of financial security and regulatory adherence.

Financial institutions, fintech companies, and other regulated businesses must implement effective KYC processes to meet regulatory requirements and manage risk. However, maintaining KYC compliance can be complex and challenging.

Balancing stringent regulations with customer experience, operational efficiency, and evolving risk factors is often challenging.

This guide provides five best practices financial institutions can adopt to strengthen their KYC compliance, mitigate risks, and improve overall regulatory adherence.

What Is KYC Compliance?

For financial entities and businesses, KYC compliance is a mandatory process to verify the identities of potential customers in an effort to mitigate financial crime. In many jurisdictions, it is also a regulatory requirement.

The goal is to prevent financial crimes such as money laundering, fraud, terrorist financing, and identity theft by verifying that customers are who they claim to be.

Financial institutions must follow strict regulations set by governing bodies like the Financial Action Task Force (FATF), Financial Crimes Enforcement Network (FinCEN), and local regulatory authorities. Non-compliance can result in hefty fines, legal penalties, and reputational damage.

Key Components of KYC Compliance

An effective KYC compliance program is built on three fundamental pillars: Customer Identification Program (CIP), Customer Due Diligence (CDD), and Ongoing Monitoring. Each plays a critical role in preventing fraud, money laundering, and other financial crimes.

1. Customer Identification Program (CIP)

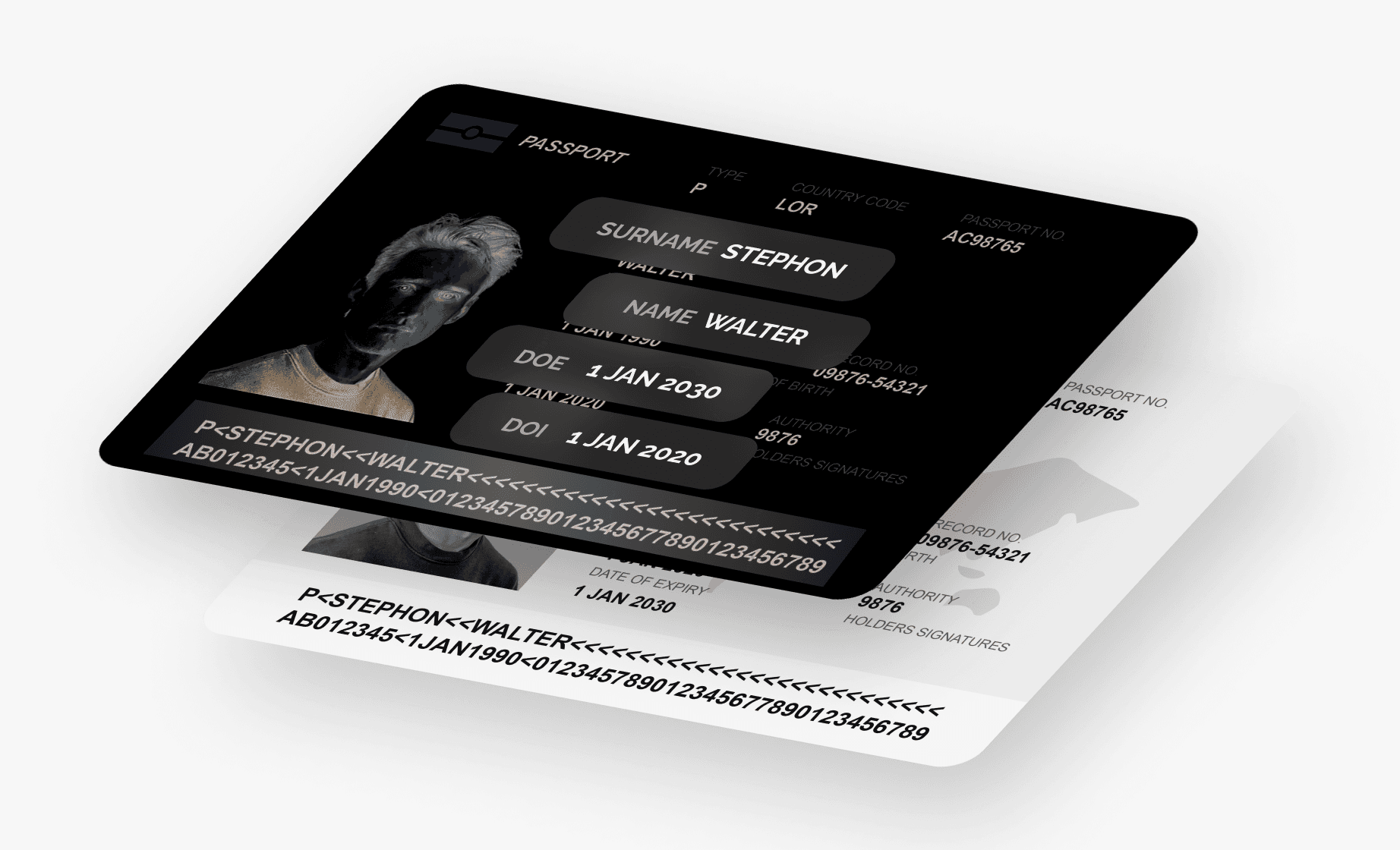

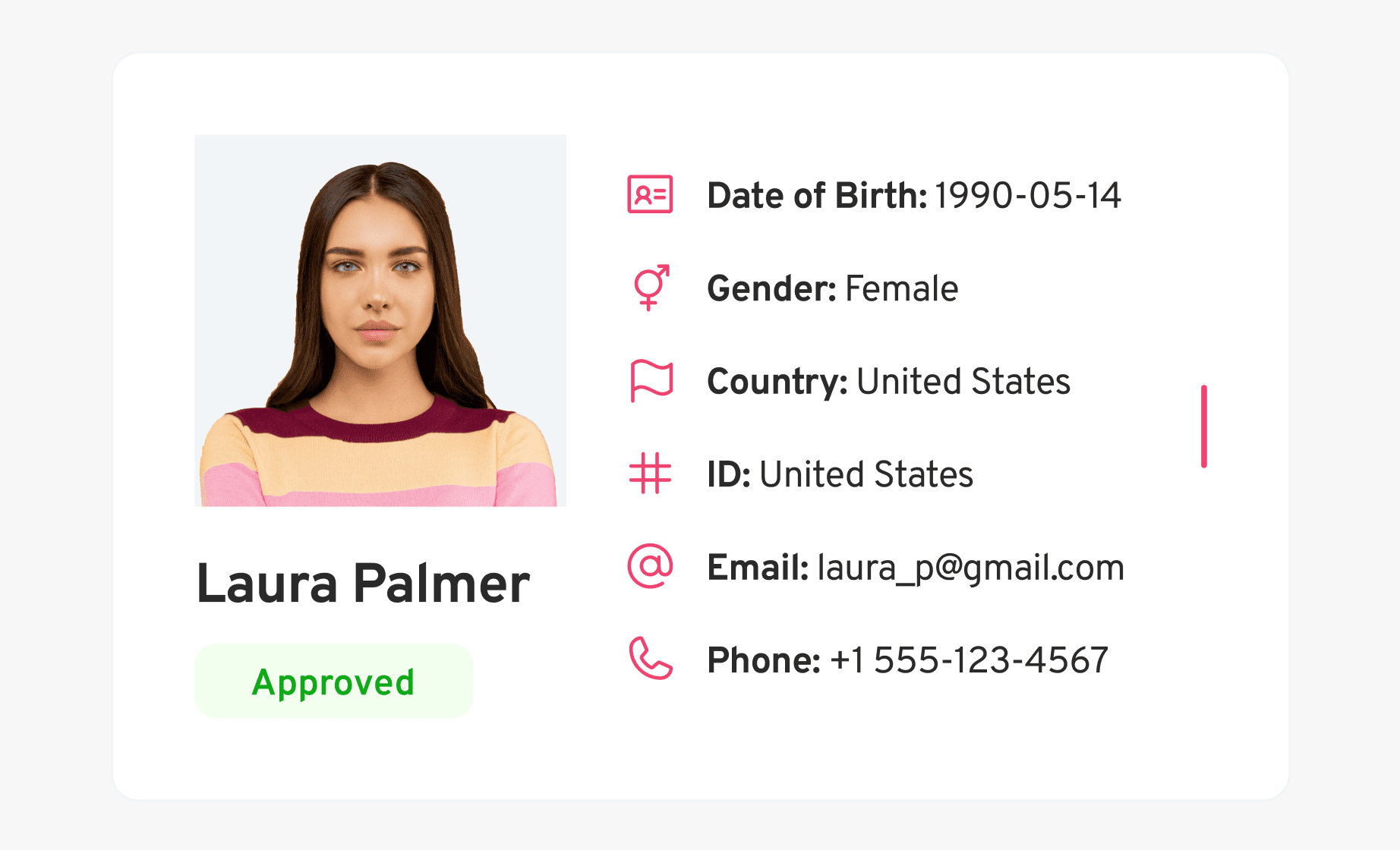

The Customer Identification Program (CIP) is the first step in KYC compliance. It requires financial institutions to collect and verify customer information before allowing them to access services.

The key requirements of CIP are:

Collecting customer information and essential identifying details, including:

Full name

Date of birth

Residential address

Unique identification number (e.g., passport, driver’s license, or national ID)

Verifying identity documents against government-issued databases or independent verification services

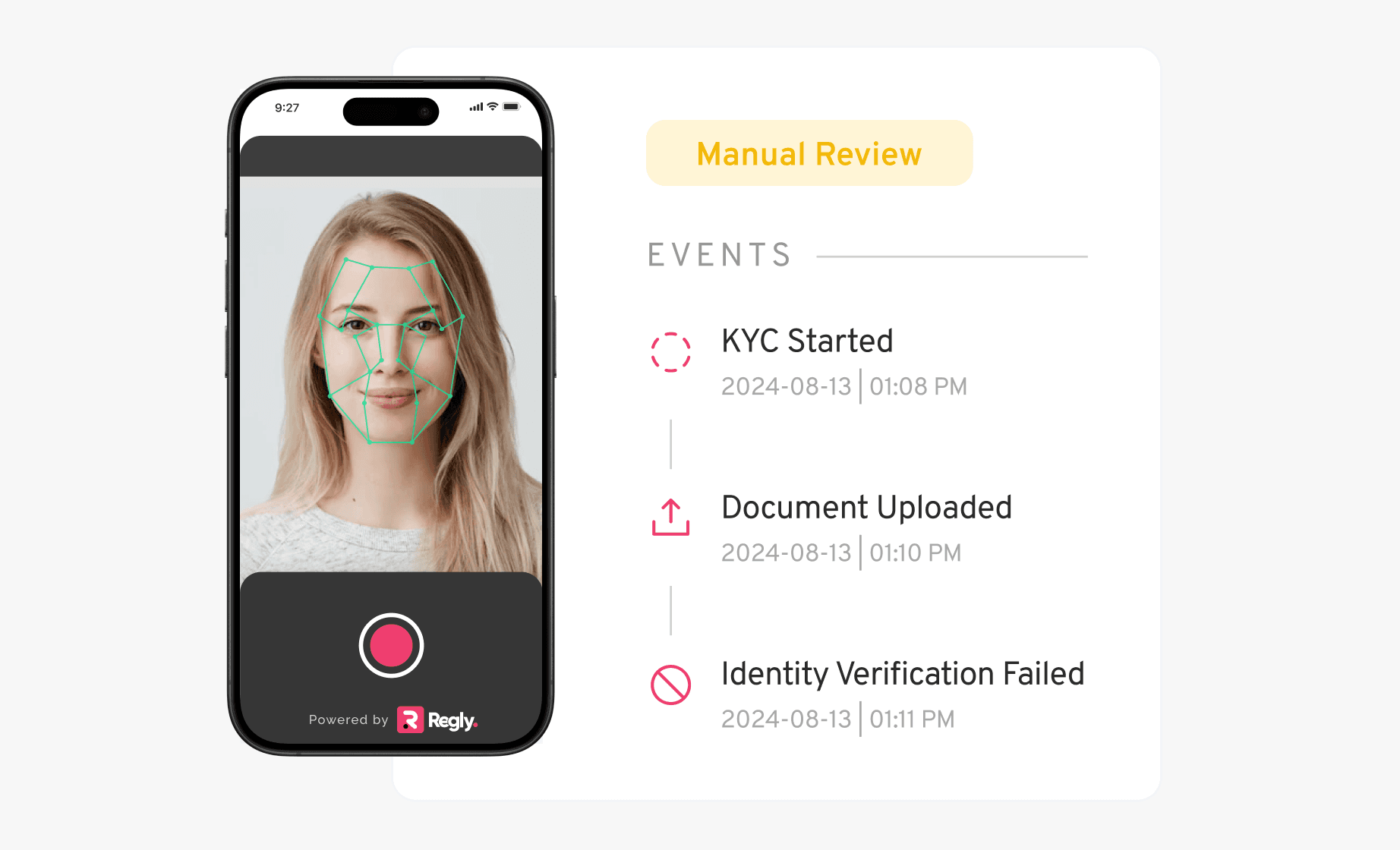

Conducting liveness detection to prevent fraudsters from using stolen or synthetic identities

Manually handling customer verification can be slow and prone to errors, leading to compliance risks and poor user experience. However, CIP tools like Regly FinCrime automate customer verification by leveraging AI-driven document checks and biometric authentication to reduce manual errors and speed up onboarding.

Regly mitigates fraud risks using real-time risk scoring and liveness detection to help verify that only legitimate users gain access.

An ineffective CIP process can expose an institution to financial crimes by onboarding fraudulent users. With Regly’s AI-driven fraud prevention tools, financial institutions can onboard customers while reducing false positives and manual work.

2. Customer Due Diligence (CDD)

Once a customer’s identity is verified, financial institutions conduct Customer Due Diligence to assess their risk profile. The goal is to understand the customer’s financial behavior and determine whether they pose a money laundering or fraud risk.

There are three main types of due diligence:

Customer Due Diligence (CDD) / Standard Due Diligence: Applied to low-risk customers with straightforward financial profiles. It involves verifying identity and assessing potential risks.

Enhanced Due Diligence (EDD): Required for high-risk customers, such as politically exposed persons (PEPs), international businesses, or entities operating in high-risk industries and/or jurisdictions. The EDD involves deeper scrutiny, ongoing monitoring, and sometimes senior management approval.

Simplified Due Diligence (SDD): Applied to situations with a low risk of money laundering or terrorist financing (e.g., for regulated entities like banks or government agencies).

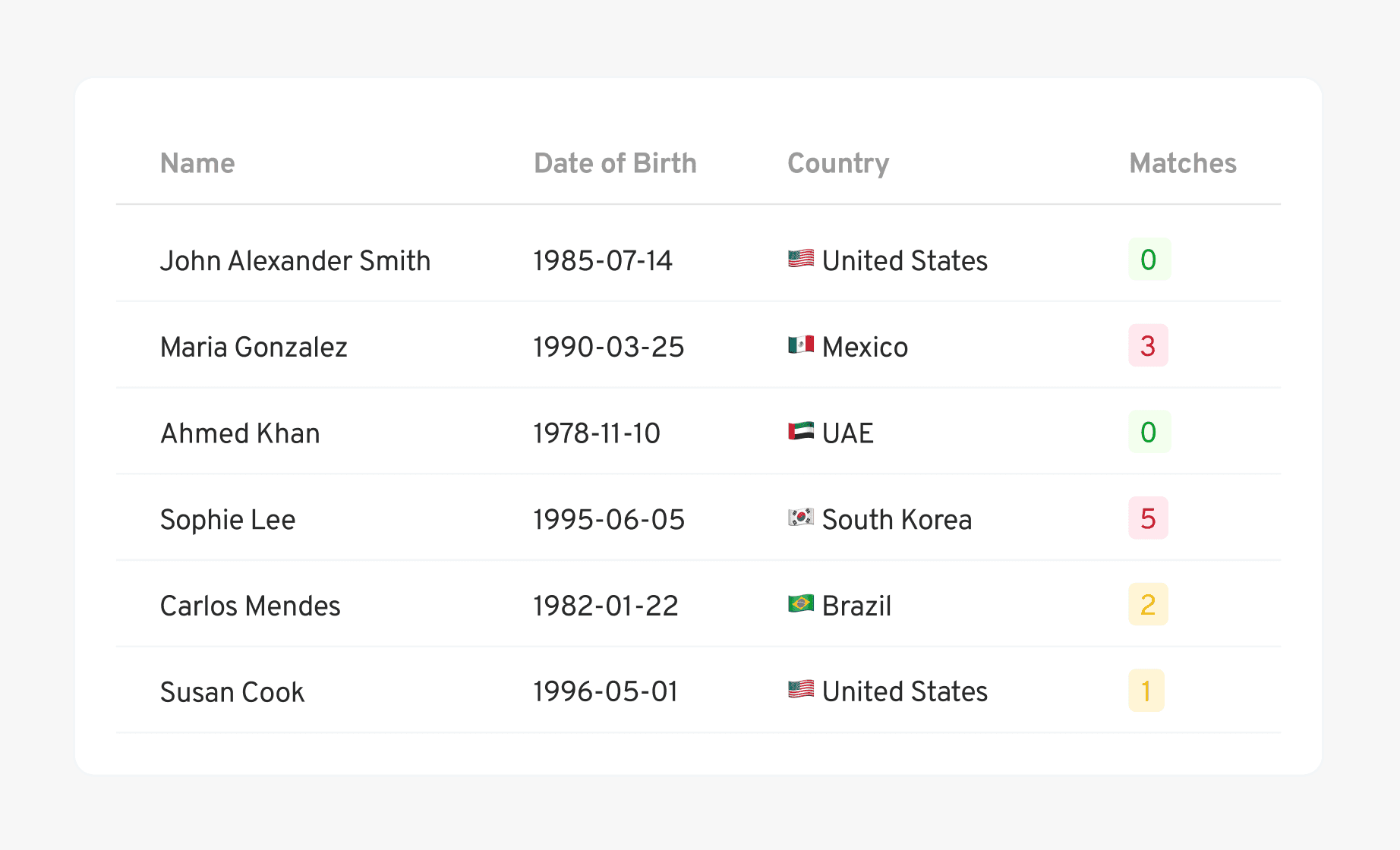

Even in low-risk cases, a comprehensive understanding of the ownership structure by applying Ultimate Beneficial Ownership (UBO) checks is essential to the broader due diligence process. Knowing who ultimately controls a business or entity is a fundamental requirement to mitigate financial crime risks.

Beyond identifying ownership, financial institutions must also verify sources of income, assess transaction behavior, and screen customers against global sanctions and watchlists to remain compliant. However, manual due diligence processes can be slow, inconsistent, and prone to errors, leading to missed red flags or unnecessary friction for legitimate customers.

Regly FinCrime automates risk profiling and due diligence. It uses AI-driven analytics to flag high-risk customers, detect hidden ownership structures, and provide real-time alerts on suspicious transactions. By continuously updating watchlist screenings and monitoring financial activity, Regly helps institutions maintain compliance without slowing down operations.

In 2023, a major financial institution onboarded a high-profile criminal due to its historically inadequate KYC procedures. Despite the bright red flags, the institution failed to conduct proper due diligence, which enabled the client to move large sums without sufficient oversight.

This case highlights the importance of strict KYC compliance to prevent financial misconduct.

3. Ongoing Monitoring

KYC compliance requires continuous customer activity monitoring to detect and report suspicious transactions. The key aspects of ongoing monitoring include:

Transaction Screening: Identifying unusual activity patterns, such as sudden large transfers or transactions in high-risk jurisdictions. Regly automates this process with AI-driven screening, enabling real-time detection without manual delays.

Behavioral Monitoring: Detecting changes in customer behavior that might indicate fraud or illicit activities.

Re-Screening Against Updated Watchlists: Customers must be regularly screened against updated sanctions lists, adverse media reports, and law enforcement alerts.

In 2018, a major US financial institution failed to detect suspicious transactions due to limitations in its automated monitoring system. The system capped daily alerts, allowing high-risk activities to go unreported.

Regulators imposed heavy penalties, highlighting the need for continuous transaction screening, behavioral monitoring, and re-screening against updated watchlists.

Top Challenges in Achieving KYC Compliance

Despite the critical role of KYC compliance in financial security, many institutions face significant challenges in implementing and maintaining effective compliance programs. Here are the key challenges they encounter.

1. Balancing Compliance with Customer Experience

Know Your Customer processes often introduce friction in user onboarding, leading to delays, abandoned applications, and customer dissatisfaction. Traditional manual verification methods can take days or even weeks, frustrating customers accustomed to fast and seamless digital experiences.

To remain competitive, financial institutions must balance compliance rigor and user convenience to reduce onboarding friction without compromising regulatory adherence.

How Regly Reduces Onboarding Friction:

Automated Identity Verification: Reduces onboarding time from days to minutes with AI-powered ID verification and biometric authentication.

Digital Document Submission: Customers can upload documents digitally, and Regly’s OCR technology extracts and verifies information instantly.

Low-Friction Compliance Workflows: Automates customer risk assessments, enabling faster approvals while maintaining compliance.

By leveraging Regly’s AI-driven identity verification, financial institutions can enhance the user experience while maintaining compliance with global regulations.

2. High Costs and Resource Demands

Implementing and maintaining a comprehensive KYC compliance program requires significant financial investment.

Financial institutions must dedicate resources to hiring and training compliance officers and fraud analysts to keep teams current with evolving regulatory demands. Additionally, they should invest in KYC verification technology and regulatory reporting tools to streamline identity verification and due diligence processes.

These ongoing compliance changes require continuous updates to policies, systems, and procedures. A mismanaged KYC process can become inefficient, leading to increased operational costs, compliance risks, and potential regulatory penalties.

How Regly Cuts Costs and Improves Efficiency:

Automation Reduces Manual Work: AI-driven risk assessments eliminate the need for manual reviews, significantly cutting compliance costs.

Scalable KYC Infrastructure: Regly’s cloud-based compliance solution allows institutions to scale without hiring additional personnel.

Built-In Regulatory Updates: Regly continuously updates watchlists, sanction databases, and compliance requirements, helping businesses anticipate regulatory changes.

By integrating Regly FinCrime, financial institutions can reduce compliance costs while improving efficiency.

3. Managing Complex and Evolving Regulatory Requirements

KYC regulations differ across jurisdictions, requiring financial institutions operating globally to navigate a complex web of compliance frameworks.

They must adhere to Anti-Money Laundering (AML) regulations, such as the Bank Secrecy Act (BSA) in the US and the EU’s AML Directives, both of which mandate stringent identity verification and transaction monitoring processes.

Additionally, institutions must comply with FATF Recommendations, which set international standards for combating money laundering and terrorist financing.

It can be a never-ending challenge to stay compliant amid these evolving and region-specific regulations, particularly for financial institutions with a multinational presence.

How Regly Simplifies Global Compliance:

Automated Compliance Updates: Regly continuously monitors and integrates new regulatory requirements, reducing the risk of non-compliance.

Multi-Jurisdictional Compliance Support: Institutions can customize KYC workflows based on region-specific AML/KYC requirements.

Real-Time Risk Scoring: AI-powered compliance tools automatically adjust customer risk scores based on new regulatory guidelines.

By using Regly’s AI-driven compliance platform, institutions can stay ahead of regulatory changes and avoid costly penalties.

4. Mitigating False Positives in Screening Processes

One of the most relentless challenges in KYC compliance is the high rate of false positives in customer screening. Many financial institutions over-flag customers due to outdated or incomplete sanctions and watchlist data, leading to unnecessary compliance reviews.

Relying on manual intervention further slows down case resolution, creating inefficiencies in compliance workflows. Additionally, poorly calibrated risk-scoring models often trigger unnecessary escalations, diverting resources away from genuine threats.

These false positives create operational bottlenecks, delaying customer onboarding and increasing compliance costs—ultimately impacting business efficiency and the customer experience.

How Regly Improves Screening Accuracy:

AI-Enhanced Screening: Regly’s machine learning algorithms intelligently reduce false positives by refining risk assessments based on behavior and transaction history.

Dynamic Risk Scoring: Instead of relying on static rules, Regly assigns real-time risk scores, improving the accuracy of customer evaluations.

Automated Case Management: Compliance teams can prioritize and resolve alerts faster, improving operational efficiency.

By leveraging Regly’s advanced fraud detection, financial institutions can reduce false positives while maintaining compliance integrity.

5. Eliminating Data Silos for a Unified Customer View

Fragmented KYC data, typically stored across disconnected systems and multiple departments, presents financial institutions with an array of significant challenges.

This siloed approach results in inconsistent and incomplete customer records, increasing the risk of non-compliance and making it difficult to maintain accurate and up-to-date information. The lack of real-time insights further complicates efforts to detect suspicious activity as compliance teams struggle to piece together a complete picture of customer behavior.

Manually reconciling data across different platforms invites operational inefficiencies, leading to delays and resource-heavy processes. Without a centralized KYC compliance platform, institutions risk overlooking critical fraud indicators and meeting regulatory requirements, exposing them to financial and reputational risks.

How Regly Unifies KYC Data for Smarter Compliance:

Unified Compliance Dashboard: Regly integrates customer data, risk scores, and transaction monitoring into a single platform for a holistic view.

Real-Time Data Synchronization: All compliance workflows, including document verification, AML screening, and ongoing monitoring, are updated instantly.

Cross-Team Collaboration: Compliance teams, fraud analysts, and risk officers can collaborate seamlessly within Regly’s AI-powered compliance suite.

By eliminating data silos, Regly provides financial institutions with a single source of truth, enhancing compliance accuracy and efficiency.

5 Best Practices for KYC Compliance

Know Your Customer is crucial for preventing fraud, money laundering, and regulatory violations. Beyond meeting legal requirements, a strong KYC process enhances security, efficiency, and customer trust.

Here are five key practices to strengthen compliance while improving operational performance.

1. Establishing Comprehensive Customer Identification Programs

An effective CIP goes beyond verifying customer identities. It is a critical safeguard against fraud, money laundering, and financial crime. A weak or outdated CIP program can allow bad actors to use false or stolen identities to exploit financial services.

Many institutions that rely on manual identity verification face high operational costs, slower onboarding times, and increased human error, all hindering compliance and customer experience.

With AI-driven document authentication and biometric verification, modern compliance solutions streamline CIP, reducing manual reviews and improving accuracy. Advanced liveness detection also prevents fraudsters from using stolen or synthetic identities, while automated cross-referencing with global databases helps detect discrepancies instantly.

2. Using Advanced Technology to Streamline KYC Processes

Traditional KYC processes can be slow, labor-intensive, and prone to errors. And financial institutions that rely on manual verification often face onboarding delays, increased compliance costs, and a higher risk of fraud slipping through the cracks.

To keep up with evolving regulations and customer expectations, institutions should adopt AI-driven solutions that enhance efficiency and accuracy.

Automated risk scoring and AI-powered identity verification allow institutions to quickly identify high-risk individuals by analyzing customer behaviors, transaction patterns, and risk indicators.

Continuous monitoring and real-time re-screening against updated sanctions lists, PEP databases, and adverse media sources also help detect potential threats before they escalate. By integrating automation into their KYC processes, financial institutions can enhance compliance while minimizing false positives and unnecessary escalations.

3. Maintaining Accurate and Up-to-Date Customer Records

KYC compliance does not end at onboarding. Continuous customer records management is required to detect changes that may indicate increased risk.

Inaccurate or outdated records can lead to compliance violations, missed fraud risks, and flawed risk assessments. To stay compliant and proactive, institutions must maintain real-time, accurate customer data.

Automated systems that synchronize customer data with global compliance databases and risk-scoring models help reduce the risk of overlooking critical updates. A centralized compliance dashboard also provides real-time insights, enabling teams to track risk trends, detect inconsistencies, and take swift action when necessary.

Additionally, real-time alerts for changes in customer details, such as addresses, financial activities, or associated risk factors, help compliance teams quickly intervene as risks emerge.

By automating record-keeping and risk monitoring, financial institutions can eliminate compliance gaps, improve due diligence, and maintain accurate customer profiles with minimal manual effort.

4. Training and Educating Teams on KYC Regulations

KYC regulations are constantly evolving, so financial institutions must keep compliance teams informed about the latest legal requirements and fraud prevention tactics. Without proper training, staff may struggle to recognize suspicious activity, misinterpret risk indicators, or follow regulatory procedures.

Integrating policy management and regulatory updates into daily workflows helps teams stay informed about new requirements and best practices. Built-in training acknowledgment tracking helps confirm that employees have reviewed and understood updated KYC guidelines.

Automated workflow tools can also guide teams through fraud investigations, risk assessments, and compliance reporting, reducing errors caused by a lack of training. By embedding compliance education into daily operations, financial institutions can develop knowledgeable teams that respond quickly and effectively to regulatory changes.

5. Conducting Continuous Risk-Based Monitoring

KYC compliance is not a one-time process. It requires ongoing risk monitoring to detect suspicious activity, prevent fraud, and maintain regulatory compliance. A risk-based approach helps institutions continuously assess customer behavior and adjust monitoring efforts accordingly.

AI-driven transaction monitoring enhances this process by analyzing transaction trends, geolocation data, and behavioral patterns to detect anomalies in real time. Automated case management allows compliance teams to review flagged transactions, escalate high-risk cases, and generate reports efficiently.

Additionally, customizable risk thresholds help align monitoring efforts with an institution’s risk appetite and regulatory obligations. By automating real-time risk analysis and fraud detection, financial institutions can proactively address compliance risks, minimize exposure to financial crime, and maintain ongoing regulatory adherence.

The Future of KYC Compliance in Financial Services

Three major trends will shape the future of KYC compliance: emerging technologies, global regulatory changes, and the shift toward seamless, risk-based compliance models.

Emerging Technologies: AI, Blockchain, and Automation

KYC compliance is undergoing a major transformation as financial institutions turn to AI, blockchain, and automation to enhance security, reduce costs, and improve efficiency. These technologies are streamlining compliance by making identity verification faster, fraud detection smarter, and regulatory adherence more seamless.

AI-powered KYC solutions analyze vast datasets in real time, identifying suspicious patterns with greater accuracy while reducing false positives and manual effort.

Blockchain technology, on the other hand, strengthens digital identity verification by allowing customers to store and share pre-verified credentials securely. This minimizes onboarding friction and improves data protection.

Automation supports continuous compliance by handling document verification, record updates, and transaction monitoring, reducing reliance on manual reviews.

Adapting to Global Regulatory Trends

KYC regulations are becoming more stringent and globally interconnected, requiring financial institutions to adopt more sophisticated compliance strategies. Regulatory bodies are introducing stricter AML guidelines, increasing due diligence requirements for high-risk customers, and imposing harsher penalties for non-compliance.

The move toward real-time compliance monitoring is a significant regulatory shift. Periodic checks are giving way to the expectation that financial institutions will continuously assess customer risk levels and detect suspicious activities in real time.

Global financial watchdogs, including FATF, FinCEN, and the EU’s AML authority, are also pushing for greater cross-border collaboration to prevent criminals from exploiting regulatory gaps across jurisdictions.

At the same time, data protection regulations such as GDPR and CCPA are forcing financial institutions to implement more secure, customer-centric compliance frameworks to balance fraud prevention with consumer privacy.

The Shift Toward Seamless, Risk-Based Compliance Models

The future of KYC compliance will be shaped by automation, AI, and regulatory adaptability. Financial institutions that integrate AI-driven identity verification, blockchain-based digital identities, and real-time risk monitoring will be better positioned to meet compliance requirements while improving efficiency.

As regulatory expectations grow, institutions must move from reactive compliance models to proactive, technology-enabled solutions that continuously monitor risks and adapt to emerging threats.

By embedding advanced technology into KYC workflows, financial institutions can stay compliant, reduce fraud risks, and enhance the customer experience to prepare for the future of financial security.

—

Know Your Customer is evolving, requiring financial institutions to move beyond manual processes and adopt technology-driven solutions for greater efficiency and accuracy. By integrating AI-powered identity verification, biometric authentication, and real-time risk monitoring, institutions can streamline compliance while enhancing fraud prevention.

Regly is at the forefront of this shift, providing automated KYC solutions and continuous compliance updates to help businesses stay ahead of regulatory changes. As the industry moves toward AI-driven, risk-based compliance, institutions that embrace advanced KYC technology will strengthen security, reduce compliance costs, and improve the customer experience.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.